Table of Contents

- What is Debt-to-Income Ratio (DTI)?

- How Personal Loans Affect DTI

- Strategies to Manage DTI Effectively

- When to Consider a Personal Loan

- Preparing for Mortgage Approval

- The Bottom Line

- Key Takeaways

- Frequently Asked Questions (FAQ)

What is Debt-to-Income Ratio (DTI)?

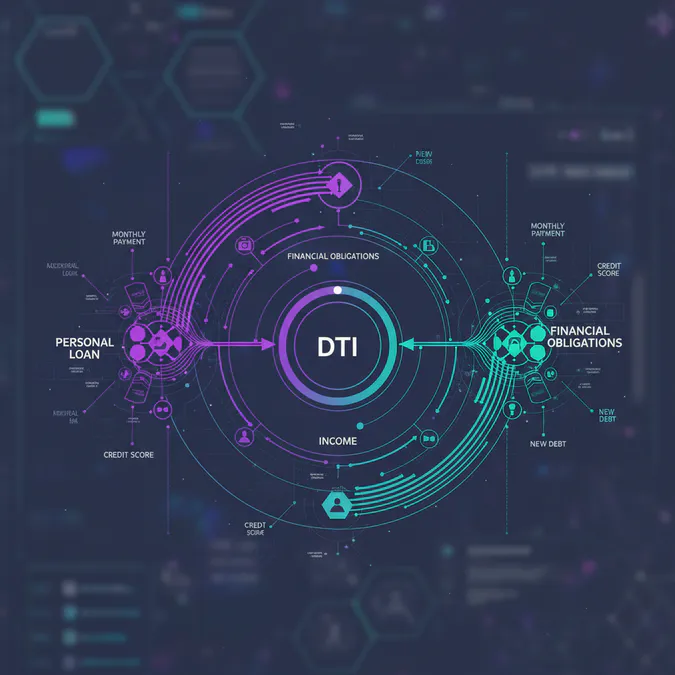

The debt-to-income ratio (DTI) is a crucial financial metric that compares an individual's total monthly debt payments to their gross monthly income. It is expressed as a percentage and is used by lenders to assess a borrower's ability to manage monthly payments and repay debts. A lower DTI indicates a healthier financial situation, making it easier to qualify for loans, including mortgages.

Calculating Your DTI

To calculate your DTI, follow these steps:

- Add up all your monthly debt payments, including credit cards, car loans, student loans, and personal loans.

- Determine your gross monthly income, which is your income before taxes and other deductions.

- Divide your total monthly debt payments by your gross monthly income and multiply by 100 to get a percentage.

For example, if your total monthly debt payments are $2,000 and your gross monthly income is $6,000, your DTI would be approximately 33%.

How Personal Loans Affect DTI

When you take out a personal loan, it typically adds a new monthly payment to your financial obligations. This increase can raise your DTI, potentially affecting your mortgage application. Here’s how:

- Increased Monthly Payments: A personal loan requires monthly payments, which are added to your existing debts. This can push your DTI higher, making you appear riskier to lenders.

- Loan Amount and Interest Rates: The amount you borrow and the interest rate on your personal loan will determine your monthly payment. Higher loan amounts or interest rates can significantly impact your DTI.

- Impact on Mortgage Qualification: Lenders typically prefer a DTI of 43% or lower for mortgage approval. If your DTI exceeds this threshold due to a personal loan, you may qualify for a smaller mortgage or face denial.

Strategies to Manage DTI Effectively

To maintain a favorable DTI and improve your chances of mortgage approval, consider the following strategies:

- Pay Down Existing Debt: Reducing your current debt can lower your DTI. Focus on paying off high-interest debts first, such as credit cards.

- Increase Your Income: Consider taking on a part-time job or freelance work to boost your income, which can help lower your DTI.

- Limit New Debt: Avoid taking on new debts, including personal loans, especially if you plan to apply for a mortgage soon.

- Consider Loan Consolidation: Consolidating multiple debts into a single loan with a lower interest rate can reduce your monthly payments and improve your DTI.

When to Consider a Personal Loan

While personal loans can impact your DTI and mortgage approval, they can also be beneficial in certain situations. Here are some scenarios where a personal loan might be a good option:

- Debt Consolidation: If you have multiple high-interest debts, a personal loan can help you consolidate them into a single, lower-interest payment.

- Emergency Expenses: Personal loans can provide quick access to funds for unexpected expenses, such as medical bills or home repairs.

- Home Improvements: If you plan to improve your home before selling or refinancing, a personal loan can finance renovations that may increase your property value.

Preparing for Mortgage Approval

To enhance your chances of mortgage approval, it’s essential to prepare adequately. Here are some steps to consider:

- Check Your Credit Score: A higher credit score can improve your chances of getting approved for a mortgage. Review your credit report for errors and work on improving your score.

- Gather Financial Documents: Lenders will require documentation of your income, debts, and assets. Prepare these documents in advance to streamline the application process.

- Consult a Financial Advisor: If you’re unsure about your financial situation, consider seeking advice from a financial advisor who can help you navigate the complexities of loans and mortgages.

The Bottom Line

Understanding how personal loans affect your debt-to-income ratio is crucial for anyone considering a mortgage. While personal loans can provide financial relief in certain situations, they can also complicate your mortgage approval process. By managing your DTI effectively and preparing for your mortgage application, you can improve your chances of securing the financing you need.

In conclusion, being informed about the implications of personal loans on your financial health is essential. By taking proactive steps to manage your debts and prepare for mortgage approval, you can navigate the lending landscape with confidence.

Key Takeaways

- Understanding personal loans and their impact on DTI is vital for mortgage approval.

- Strategies like debt reduction and income increase can help manage DTI.

- Personal loans can be useful for debt consolidation and emergency expenses.

- Preparing your financial documents and checking your credit score is essential for mortgage readiness.

Frequently Asked Questions (FAQ)

1. How do personal loans affect my credit score?

Personal loans can impact your credit score positively if you make timely payments, but they may lower your score temporarily when you apply due to the hard inquiry.

2. Can I get a mortgage with a personal loan?

Yes, you can still get a mortgage with a personal loan, but it may affect your DTI and the amount you can borrow.

3. What is a good DTI ratio for mortgage approval?

A DTI ratio of 43% or lower is generally preferred by lenders for mortgage approval.

Additional Resources

For more information on personal loans and managing your finances, consider visiting reputable financial websites such as Consumer Financial Protection Bureau or Bankrate.